Businorem ipsum dolor sit amet cons interdum quam duis variuy time honored tradition etting .

Businorem ipsum dolor sit amet cons interdum quam duis variuy time honored tradition etting .

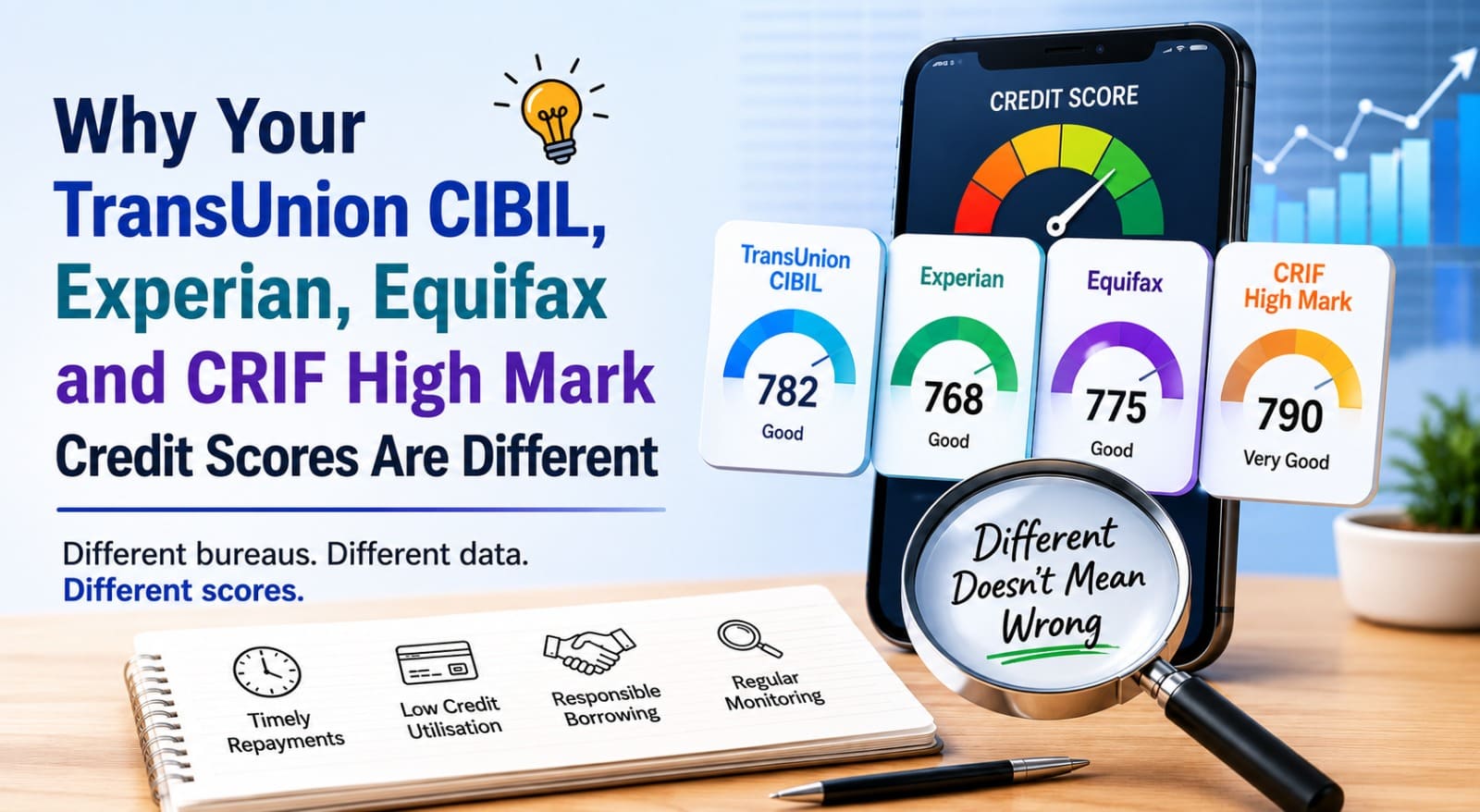

Many borrowers are surprised when they check their Credit Scores across different Credit Bureaus and notice that the numbers do not match. A person may simultaneously have a 782 with TransUnion CIBIL, 768 with Experian, 775 with Equifax, and 790 with CRIF High Mark. This is completely normal. In India, all four RBI-authorised Credit Bureaus maintain their own databases, reporting structures, and scoring methodologies. While each bureau evaluates your creditworthiness, they may interpret the same financial behaviour differently, leading to variations in Credit Scores.

One of the primary reasons for these differences is that every Credit Bureau uses its own proprietary scoring model. Even when the underlying repayment behaviour remains the same, the importance assigned to factors such as repayment history, credit utilisation, age of accounts, loan mix, and recent enquiries may vary from one bureau to another. In some cases, certain loan accounts, especially those related to smaller NBFCs, fintech lenders, or older credit facilities, may also be interpreted differently across bureaus.

Credit Scores are dynamic and change whenever new information is reported. Even checking your Credit Reports a few days apart can lead to score differences due to fresh repayments, balance updates, or recent credit enquiries being captured by one bureau before another.

In addition, the completeness of your credit history may vary across Credit Bureaus depending on how lenders have historically reported your data. Missing, delayed, or partially updated information related to loans, credit cards, or repayment behaviour can directly influence the Credit Score generated by each Credit Bureau.

However, a Credit Score difference of 20 to 40 points across bureaus is generally not considered a concern. Lenders themselves often rely on different Credit Bureaus depending on their internal underwriting policies and credit assessment frameworks. Instead of focusing on maintaining identical scores across all bureaus, borrowers should concentrate on building healthy credit behaviour over time. Consistent repayments, controlled credit utilisation, responsible borrowing, and regular monitoring of Credit Reports play a much larger role in strengthening overall creditworthiness.

At Athena CredXpert, we believe that understanding the factors shaping your credit profile is far more important than fixating on a single Credit Score. Ultimately, a Credit Score is only a reflection of financial behaviour, and informed financial habits remain the strongest foundation for long-term credit health.