Businorem ipsum dolor sit amet cons interdum quam duis variuy time honored tradition etting .

Businorem ipsum dolor sit amet cons interdum quam duis variuy time honored tradition etting .

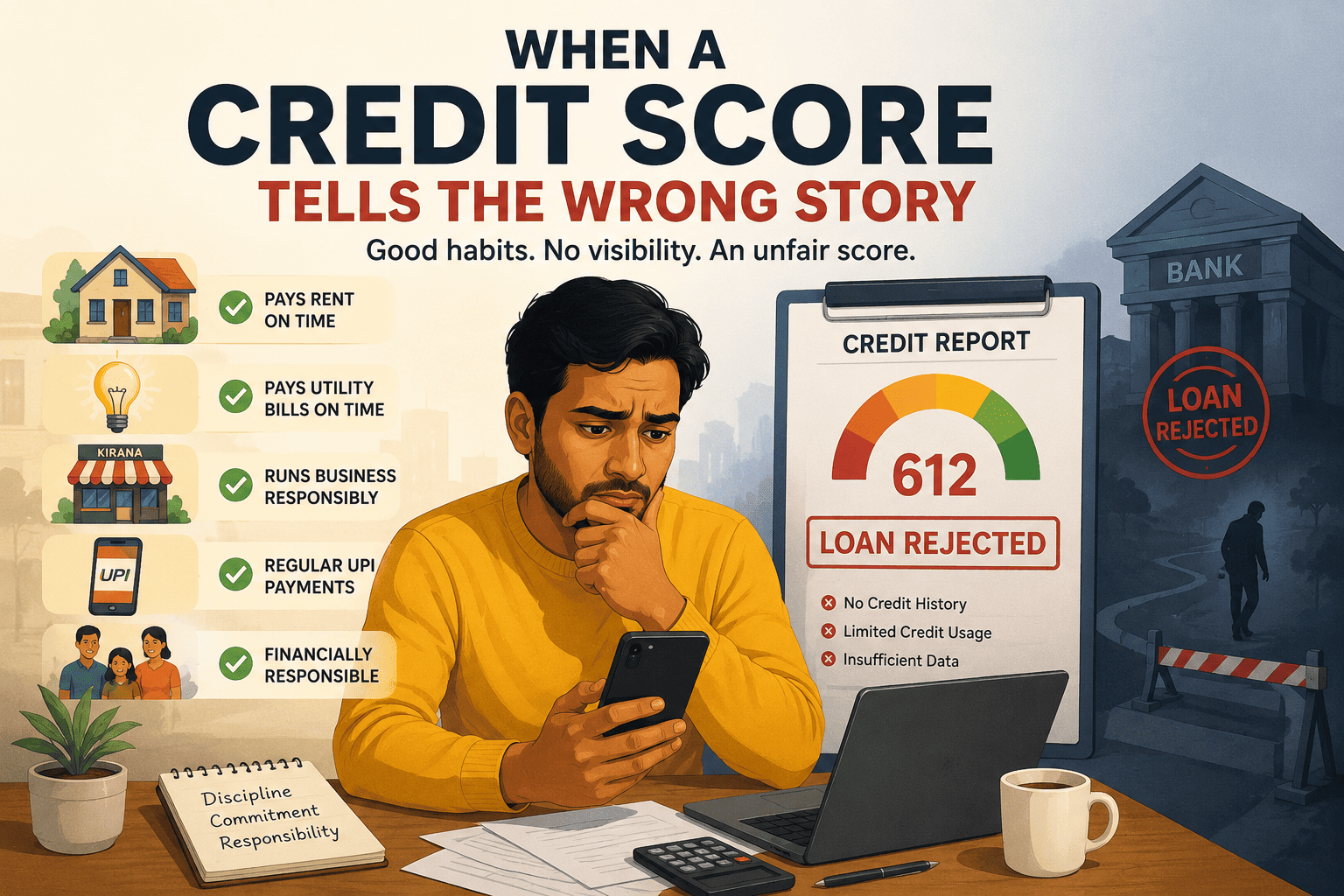

Millions of financially responsible people carry numbers that do not reflect who they truly are. Here is why and what to do about it.

Imagine being turned down for a home loan not because you missed an EMI, but because you paid rent in cash, ran a business on informal credit, or simply never needed to borrow from a bank. Your financial behaviour was responsible. But the number said otherwise.

In India, a Credit Score has become the gatekeeper to formal financial life, determining whether you qualify for a home loan, a credit card, or sometimes even a rental agreement. Yet the system behind that number has serious blind spots that leave crores of Indians either mischaracterised or completely invisible.

A Credit Score does not measure whether you are good with money. It measures how much you have used credit and in what specific ways. The gap between behaviour and score is significant. Credit scoring in India is built on a narrow slice of a person’s financial life: loans, credit cards, and repayment histories reported by formal lenders. What it misses is enormous, especially in a country where a large part of economic activity still happens informally.

Rent payments, which are often the largest monthly expense for urban Indians, usually go unrecorded. Years of paying utility bills on time leave no trace in a credit history. A kirana store owner, freelancer, gig worker, or small trader who has never defaulted on any obligation may still be treated as “credit unknown” by formal lenders simply because their financial behaviour is not visible to Credit Bureaus.

India’s vast informal workforce, including daily wage earners, traders, farmers, and gig workers, is particularly affected. Many participate in a financial ecosystem that Credit Bureaus simply cannot fully capture. They may be financially disciplined and reliable, yet arrive at a bank with little or no formal credit footprint.

This creates a difficult cycle. If you have never taken out a loan, banks may hesitate to lend to you because you have no repayment history. But without a loan, it becomes difficult to build that track record in the first place. Fresh graduates, young professionals, and people from smaller towns where formal banking penetration has historically been lower often face this challenge.

People who have experienced financial hardship, such as a medical emergency, crop failure, job loss, or business setback, may also continue to carry the impact long after recovering financially. A single default can remain on the Credit Report for up to seven years, even if every payment afterwards has been made on time.

There are several reasons why a Credit Score may not accurately reflect someone’s financial reality in India. Rent payments, utility bills, and mobile recharges are generally not reported to Credit Bureaus. Informal borrowing, chit funds, and loans from friends or family leave no positive credit trail. Acting as a guarantor for someone else’s loan can hurt your own Credit Score if that borrower defaults. Errors caused by incorrect reporting or identity mismatches are also more common than many people realise. Settled accounts are viewed almost as negatively as defaults, and multiple loan enquiries made while comparing interest rates may also reduce a score. In some cases, repayment histories from NBFCs or microfinance institutions may not fully appear if the lender reports data to only one Credit Bureau.

Errors in credit records are another major concern. Lenders sometimes report incorrect balances, fail to update closed accounts, or continue showing settled loans as unpaid. Mistakes involving names, addresses, or dates of birth can even merge one person’s file with another’s. Under RBI guidelines, every Individual is entitled to one free Credit Report each year from all four Credit Bureaus. Yet most Indians have never checked their Credit Report even once. The responsibility of identifying and disputing errors still largely falls on consumers, and the correction process can take time and persistence.

The system, however, is slowly evolving. The RBI has been encouraging lenders to move beyond traditional Credit Bureau-based scoring models. Fintech companies increasingly use GST records, UPI transaction history, rent payments, and cash-flow analysis to assess creditworthiness. The Account Aggregator framework allows Individuals, with their consent, to share financial data securely so lenders can better understand banking behaviour such as salary credits, savings patterns, and recurring payments. For rural borrowers and microfinance customers, specialised Credit Bureaus like CRIF High Mark are already capturing repayment histories that traditional systems may miss.

There are practical steps consumers can take to improve their credit profile. Checking your Credit Reports regularly from all four Credit Bureaus is important. Errors should be disputed formally and documented carefully. For people starting from zero, a secured credit card backed by a fixed deposit is often the easiest way to begin building a credit history. Co-applying for a loan with a financially reliable family member can also help establish credibility. Some platforms now allow rent payments to be voluntarily reported to Credit Bureaus.

A Credit Score reflects only one part of a person’s financial life. Understanding its limitations is the first step toward taking back control of your financial identity.