Businorem ipsum dolor sit amet cons interdum quam duis variuy time honored tradition etting .

Businorem ipsum dolor sit amet cons interdum quam duis variuy time honored tradition etting .

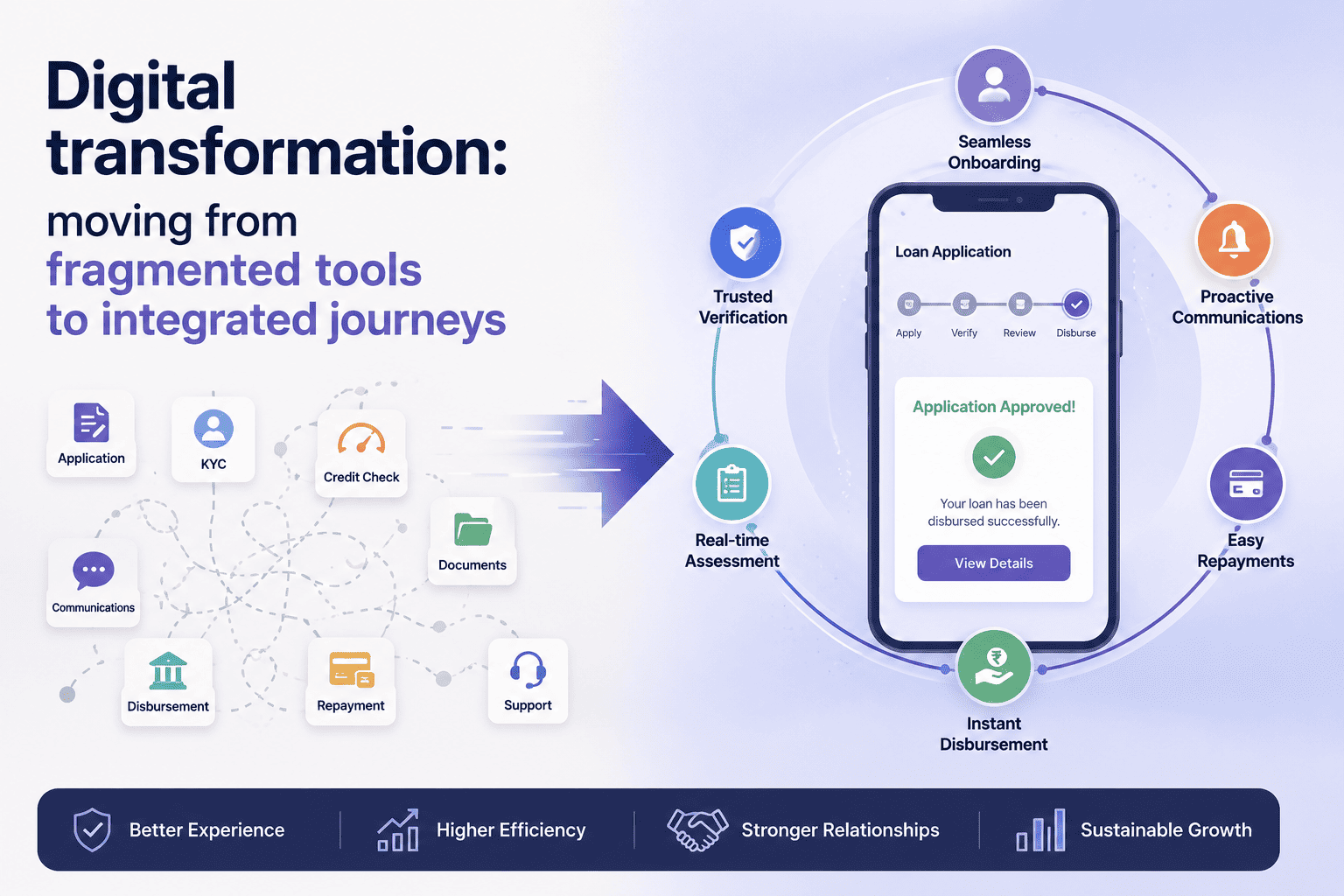

Digital transformation is often spoken of as if it were an achievement already in motion, a steady march toward efficiency and intelligence. The language is confident, the intent appears clear. Yet, beneath that assurance lies a more unsettling truth. The industry is not short of technology. It is short of coherence. And until that imbalance is addressed, can transformation claim any real meaning?

Across lending institutions, fragmentation has not diminished. It has evolved. Tools have multiplied, interfaces have improved, and data has become richer. But the journey remains disjointed. A loan still travels through islands of decision-making, each system capturing a fragment, each team owning a piece. The result is not just inefficiency, but a dilution of accountability. When everything is connected superficially, nothing is truly owned.

This is no longer a technical inconvenience. It is a structural risk. Fragmentation distorts credit decisions, delays response times, and obscures early warning signals. It creates an environment where problems are discovered late and explained away earlier. And yet, institutions continue to invest in additional layers, as if accumulation alone will resolve what is fundamentally a problem of design.

The need now is not for incremental fixes, but for deliberate reconstruction. The industry must move from asking how to improve existing systems to questioning whether those systems should exist in their current form at all. Why should a borrower’s data be entered multiple times? Why should underwriting depend on reconciliations across platforms? Why should monitoring operate on information that is already outdated by the time it is accessed?

An integrated journey is not a technological luxury. It is an operational necessity. But achieving it requires more than connecting systems. It demands a redefinition of ownership. The lending lifecycle cannot be divided into isolated domains where each function optimizes for its own metrics. Someone must own the continuity of the journey, from the first interaction to the final repayment or recovery. Without that ownership, integration remains an abstraction.

There is also a need to confront legacy thinking. Institutions often defend fragmentation as a byproduct of scale, as an inevitable outcome of growth. That argument no longer holds. Scale without integration amplifies inefficiency. Growth without alignment magnifies risk. The question is not whether legacy systems can be preserved, but whether they can justify their place in a future that demands speed with clarity.

Solutions, therefore, must begin with simplification. Not cosmetic simplification, but structural. Systems must be evaluated not by their individual performance, but by their contribution to the journey as a whole. Redundant processes must be eliminated, not automated. Data must have a single source of truth, not multiple versions of convenience. And decision-making must be anchored in a real-time context, not retrospective reconciliation.

Equally important is the alignment of incentives. As long as teams are rewarded for isolated outcomes, fragmentation will persist. Sales will prioritize volume, operations will prioritize throughput, and risk will prioritize containment. Each objective is valid in isolation, but together they create conflict. Integration requires a shared definition of success, one that values the quality and continuity of the entire journey over the performance of individual stages.

Technology, of course, has a critical role to play. But its role must be reframed. It is not the centerpiece of transformation, but its enabler. The focus should shift from acquiring tools to architecting experiences. From building capabilities to orchestrating them. From managing data to understanding it as a continuous flow.

There is also a cultural shift that cannot be ignored. Transparency must replace tolerance for ambiguity. When inconsistencies appear, they must be resolved at their source, not absorbed downstream. When gaps are identified, they must trigger correction, not accommodation. Integration thrives in environments where clarity is enforced, not negotiated.

The cost of inaction is no longer subtle. It is visible in rising operational overheads, in inconsistent customer experiences, and in risks that materialize without warning. More importantly, it is visible in lost opportunity. In an era where agility defines competitiveness, fragmentation becomes a constraint that institutions can no longer afford to carry.

So the question before the industry is not whether it recognizes the problem. That recognition is already widespread. The question is whether it is prepared to act with the urgency that the problem demands. Will institutions continue to refine the edges of fragmentation, or will they confront its core?

Because digital transformation, if it is to mean anything, must go beyond the adoption of tools. It must become an exercise in discipline. In choosing integration over convenience, clarity over complexity, and ownership over diffusion. Until that shift occurs, the promise of transformation will remain intact in language, but absent in reality.