Businorem ipsum dolor sit amet cons interdum quam duis variuy time honored tradition etting .

Businorem ipsum dolor sit amet cons interdum quam duis variuy time honored tradition etting .

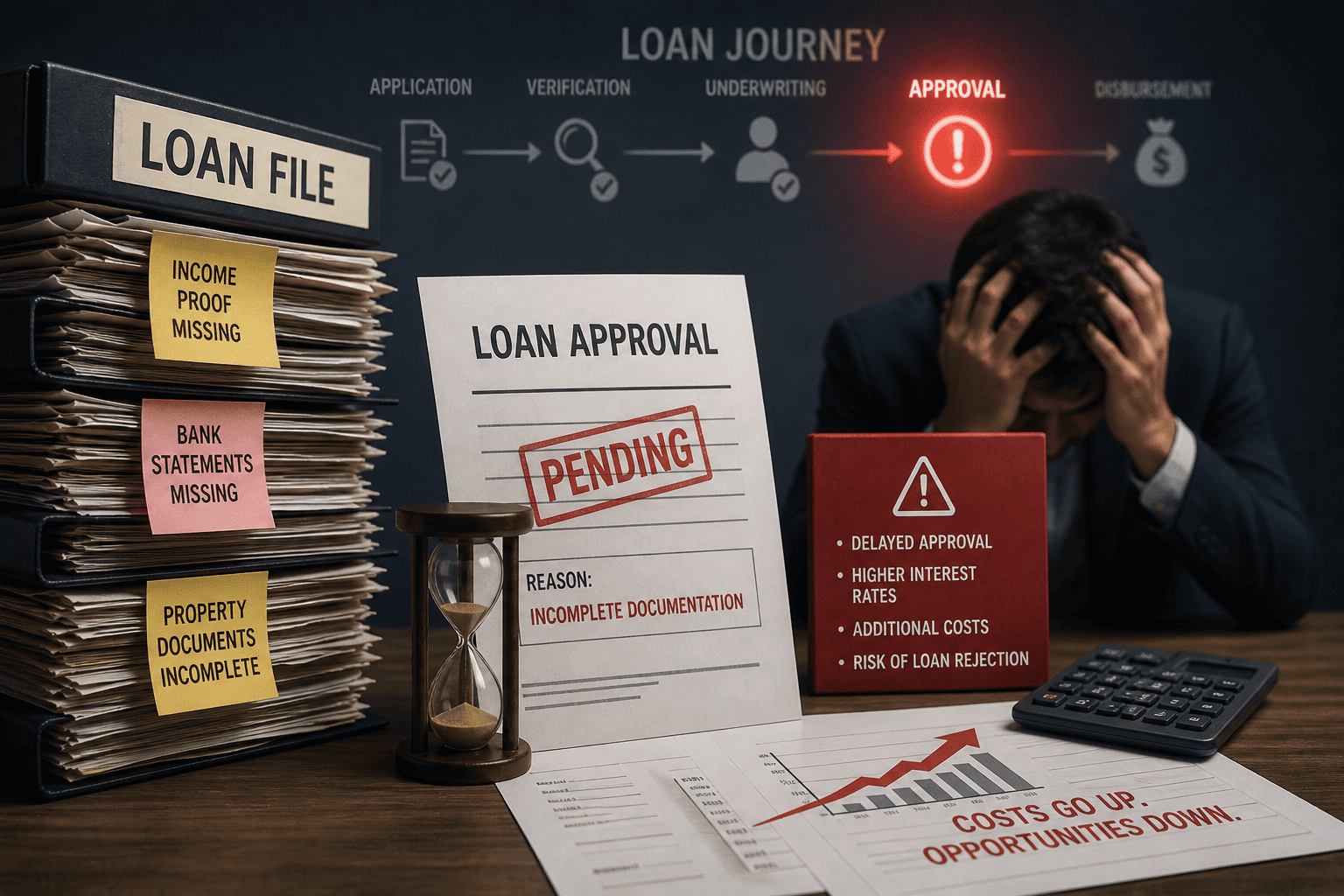

In many lending institutions, the pressure to accelerate disbursements, driven by growth targets, competitive intensity, and client expectations, has led to a normalization of “document-light” originations. Files are approved with pending conditions, deviations are informally accepted, and documentation gaps are parked for post-disbursement closure. While operationally convenient in the short term, this practice embeds a structural weakness into the loan from day one.

Incomplete documentation at origination is not a timing issue; it is a deferred liability. The associated costs do not disappear; they migrate forward and amplify across the lifecycle, often surfacing at the most value-sensitive stages such as monitoring, restructuring, or recovery. For lenders operating at scale, this translates into a measurable erosion of profitability and risk control.

Following are some of the implications of an incomplete loan file at later stages:

1. Front-Loaded Revenue vs. Back-Loaded Cost

The immediate benefit of relaxed documentation at origination is clear: faster turnaround times and accelerated revenue recognition. However, this is typically offset by a series of downstream costs that are both recurring and compounding.

Loans originated with pending documentation require ongoing tracking, borrower follow-ups, and exception management. Operations and credit teams expend disproportionate effort “closing the loop” on gaps, increasing cost-to-operate per account. In high-volume portfolios, this creates a structural cost layer that is rarely attributed back to origination decisions, masking the true economics of growth.

More importantly, a portion of these gaps never get resolved. Over time, this leads to a persistent stock of “documentation-deficient” accounts, each carrying latent risk and operational overhead.

2. Structural Weakening of Credit Risk Controls

Incomplete documentation at origination directly compromises the integrity of credit assessment. Missing financial disclosures, unverified income proofs, or incomplete collateral records result in underwriting decisions based on partial information.

This creates two cost implications:

· Systematic risk mispricing: Loans are approved without a full understanding of borrower risk, leading to underestimation of probability of default (PD) and loss given default (LGD).

· Distorted portfolio signals: As these accounts season, their performance skews portfolio analytics, making it harder to distinguish between genuine credit deterioration and origination-driven weaknesses.

The result is a gradual but tangible increase in credit costs, often misattributed to macroeconomic factors rather than origination discipline.

3. Collateral and Security Imperfections

One of the most consequential risks of incomplete origination documentation lies in imperfect security creation. Missing title verifications, unregistered charges, or incomplete collateral documentation can render security interests legally weak or, in extreme cases, unenforceable.

The financial impact becomes acute in default scenarios. Recovery assumptions embedded at the time of underwriting, often based on secured exposure, prove optimistic when enforcement is challenged, leading to:

· Lower-than-expected recovery rates

· Higher write-offs and provisioning

· Extended resolution timelines, increasing carrying costs

In effect, the lender bears unsecured risk on what was priced as a secured loan.

4. Legal Remediation and Rectification Costs

Attempting to rectify documentation gaps post-disbursement is both expensive and uncertain. Borrowers have limited incentive to comply once funds are released, particularly in stressed situations. Legal teams are then required to reconstruct or regularize documentation, often involving re-execution of agreements, additional filings, or retrospective compliance measures.

These efforts incur direct legal costs, consume internal bandwidth, and frequently deliver suboptimal outcomes. In many cases, gaps remain only partially addressed, leaving residual enforceability risk.

5. Regulatory and Audit Implications

From a regulatory standpoint, origination-stage deficiencies are viewed more critically than lifecycle gaps, as they indicate weaknesses in underwriting discipline and control frameworks. Audit findings related to incomplete documentation at sanction or disbursement stages can trigger:

· Financial penalties or supervisory observations

· Mandated remediation exercises across portfolios

· Increased scrutiny on credit processes and governance

Additionally, such deficiencies can influence internal and external audit ratings, indirectly affecting funding costs and stakeholder confidence.

The persistence of incomplete documentation at origination is typically driven by misaligned incentives. Sales and business teams are rewarded for disbursement volumes, while the cost of documentation gaps is absorbed later by operations, risk, and legal functions. In the absence of closed-loop accountability, institutions systematically trade long-term cost for short-term growth.

Leading lenders are addressing this issue by quantifying the lifecycle cost of documentation gaps and embedding this into origination governance. This includes stricter pre-disbursement controls, digitized document capture and validation, and linking documentation completeness to approval authority and performance metrics.

The objective is not to slow down origination, but to eliminate avoidable downstream cost and risk.

Incomplete documentation at origination is a high-impact, low-visibility cost driver. What appears as a minor deviation at the point of sanction can translate into sustained operational inefficiencies, elevated credit losses, impaired recoveries, and regulatory exposure over the life of the loan. These costs are cumulative and often irreversible.

For lenders focused on sustainable growth, the priority must shift from speed alone to disciplined, documentation-complete origination. Institutions that embed this rigor will not only reduce hidden costs but also enhance the reliability of their credit portfolios and the resilience of their operations.

Athena Advisors partners with financial institutions to eliminate the hidden costs embedded in origination practices. The firm conducts detailed diagnostics to quantify the downstream financial impact of documentation gaps, linking origination decisions to lifecycle performance.

We support the design of robust, front-loaded documentation frameworks, integrates digital document management and validation tools, and aligns incentives across business, credit, and operations teams to enforce completeness at source. The firm also helps establish governance mechanisms, such as pre-disbursement control checklists and exception tracking systems to prevent leakage.

By shifting documentation discipline upstream, Athena Advisors enables lenders to reduce cost-to-operate, improve credit outcomes, and build more resilient, scalable lending operations.