Businorem ipsum dolor sit amet cons interdum quam duis variuy time honored tradition etting .

Businorem ipsum dolor sit amet cons interdum quam duis variuy time honored tradition etting .

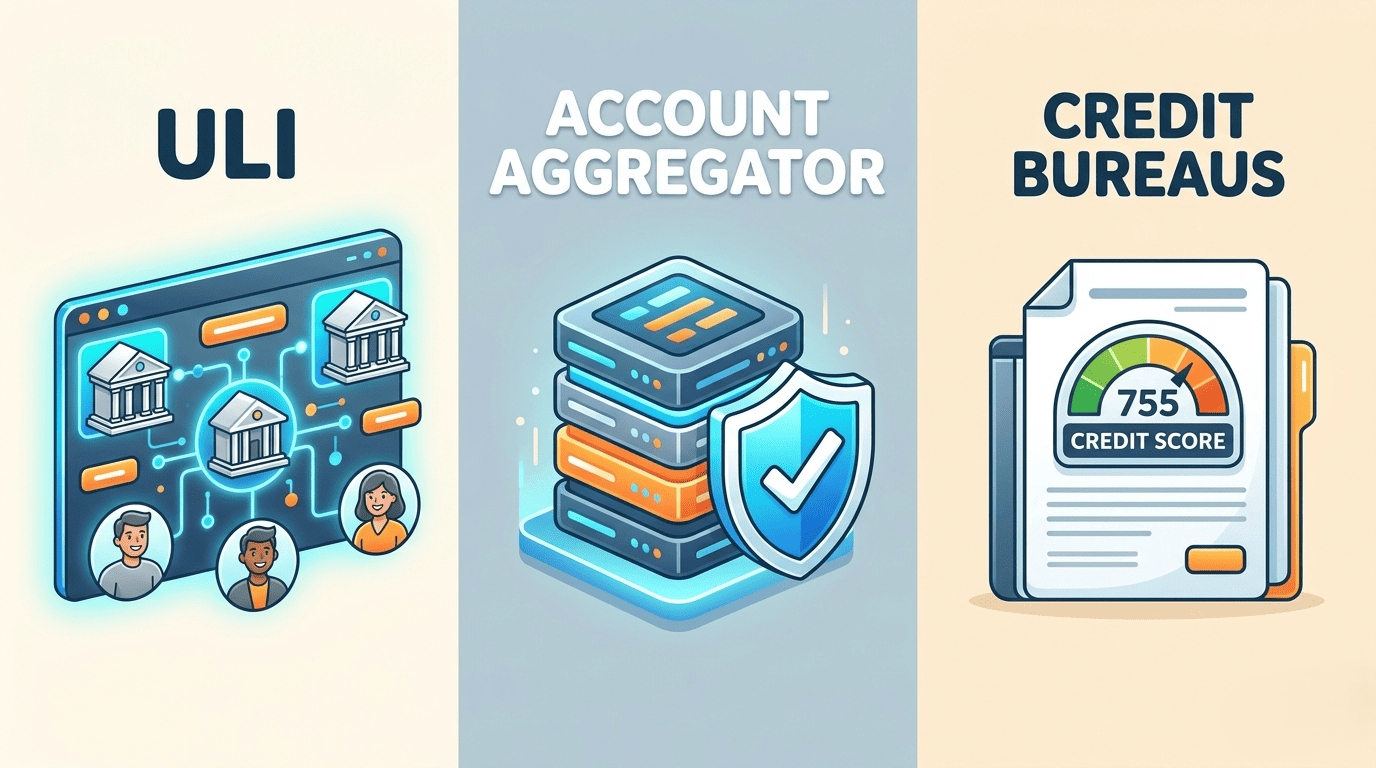

Over the last decade, India’s lending ecosystem has evolved from paperwork-heavy processes to a data-driven infrastructure. Yet, conversations across boardrooms and policy forums still frame Account Aggregator (AA), Unified Lending Interface (ULI), and Credit Bureaus as separate or even competing innovations.

From Credit History to Credit Intelligence

Traditional credit underwriting relied heavily on Credit Bureau data – a retrospective view of borrower behaviour. Credit Reports built the foundation of risk assessment, enabling lenders to evaluate repayment patterns.

But credit history alone has limitations. In a dynamic economy where income patterns shift quickly, static data cannot fully capture financial capacity. This is where the ecosystem is evolving:

One Loan Application, Three Systems

Imagine borrower wants a business loan.

· The lender checks borrower’s past credit history – this comes from a Credit Bureau.

· The lender wants borrower’s latest bank transactions and income proof – this comes through an AA with borrower’s consent.

· The lender uses a digital platform to connect data, process the loan faster, and manage approvals this is where the ULI comes in.

Each system solves a different problem, but together they make lending faster and more transparent.

From data silos to intelligent lending – understanding the new credit stack.

Credit Bureaus, remain the foundation representing historical insight into repayment behaviour. Credit Bureaus answer one critical question: Has the borrower paid in the past?

While Credit Bureau data is powerful, it reflects the past. In a fast-changing economy, relying solely on historical behaviour can limit financial inclusion – especially for non-individuals and new-to-credit borrowers.

AA, regulated by the Reserve Bank of India, add a new dimension by enabling consent-based sharing of real-time financial data.

AA does not replace Credit Bureaus; it complements. Where Credit Bureaus answer “Has this borrower repayed in the past?”, AA helps answer “Can this borrower pay today?”.

ULI, is a digital infrastructure that standardises and connects lenders, data sources, and platforms to enable faster, seamless, and scalable loan processing. ULI represents the shift from isolated lending platforms to network-driven credit ecosystems. It allows multiple data layers – including Credit Bureau and AA, to be integrated seamlessly.

Strategic implications for the ecosystem

For Lenders

· Combining Credit Bureau data with AA insights improves credit underwriting accuracy.

· ULI reduces operational friction and enhances scalability.

For Borrowers

· Transparency increases, but so does accountability.

· Real-time cashflow visibility means financial discipline matters more than ever.

As innovation accelerates, so do the misconceptions surrounding these frameworks. Credit Bureau data remains as critical as ever, historical repayment behaviour continues to be a foundational input in credit decisioning, regardless of how data is sourced or shared. The Account Aggregator framework does not improve a borrower’s credit score, it simply enables consented sharing of financial data between institutions. Similarly, the Unified Lending Interface does not sanction or reject loans , that decision remains entirely with the lender.

India is moving toward a future where lending decisions are no longer based on a single dataset. Instead, they rely on a multi-layered intelligence model:

· Credit Bureaus provide historical credibility – anchoring the lender’s view of a borrower’s past repayment behaviour and long-term credit worthiness.

· Account Aggregators bring real-time financial context – giving lenders a consented, current view of a borrower’s income, cash flows, and existing obligations.

· The Unified Lending Interface delivers operational efficiency – streamlining the end-to-end lending process by connecting data, decisioning, and disbursement on a single interoperable infrastructure.

The future of lending is not about choosing between Credit Bureau, AA & ULI – it is about how effectively they work together to create faster, fairer, and more inclusive access to credit.

The reality is far more strategic: these are not parallel systems – they are layers of a single digital credit architecture that is reshaping how trust, risk, and inclusion are defined.

The real power lies in integration, not substitution.