Businorem ipsum dolor sit amet cons interdum quam duis variuy time honored tradition etting .

Businorem ipsum dolor sit amet cons interdum quam duis variuy time honored tradition etting .

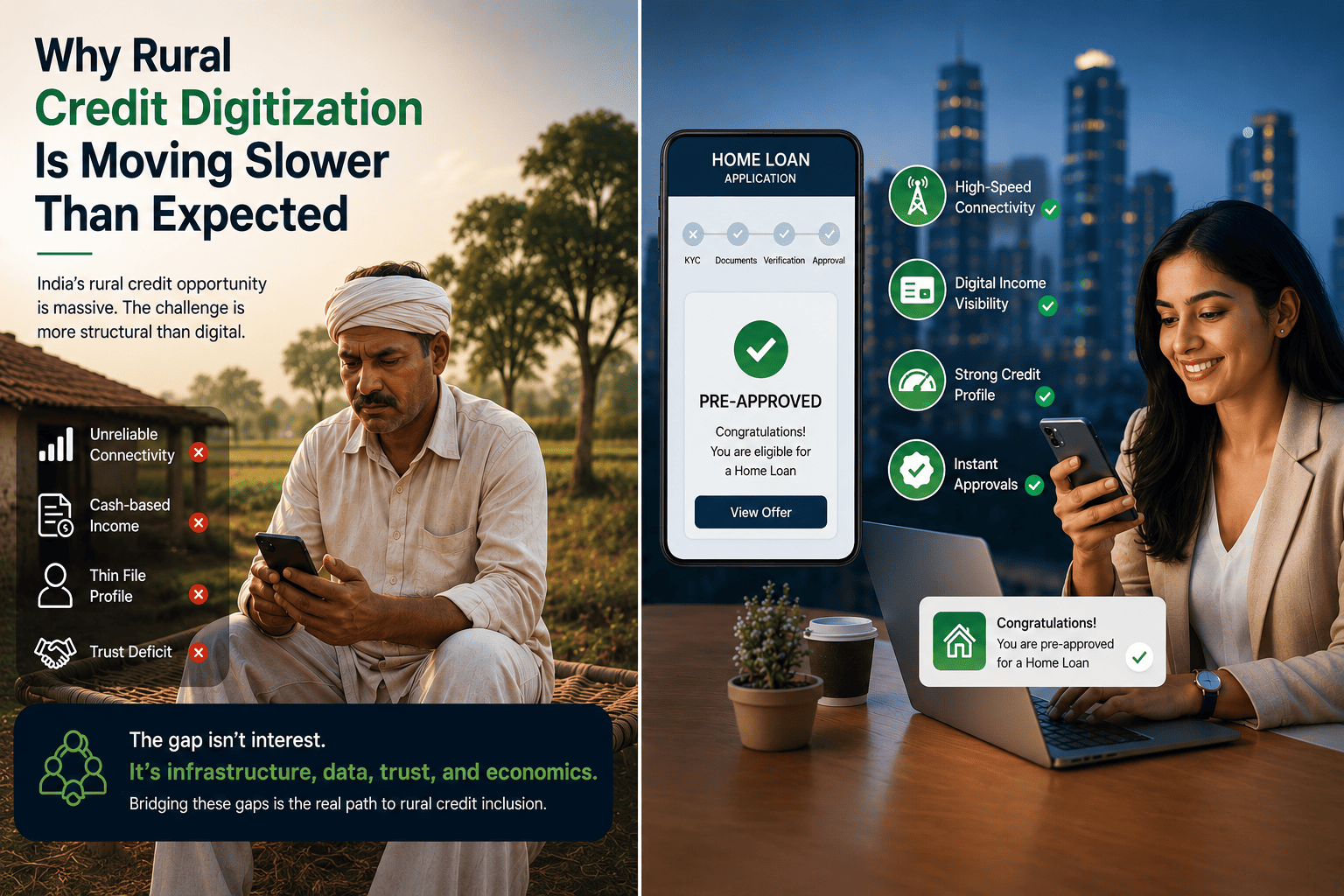

Why Rural Credit Digitization Is Moving Slower Than Expected

A small farmer in Vidarbha earns steadily across three seasons, repays his informal lender on time every cycle, and holds clear title to four acres of land. When he walks into a branch to apply for a housing loan, the process stalls within days. His bureau file is thin. His income is cash-based. His documentation does not match the underwriting model. He leaves empty-handed.

Meanwhile, a salaried professional in Pune receives three pre-approved offers on her phone before she even searches for one.

Both outcomes share a common cause: digital lending was designed around urban borrower profiles, urban infrastructure, and urban data availability.

India’s rural credit market represents one of the largest underserved opportunities in financial services. HFCs, NBFCs, and fintech lenders have spoken about Bharat penetration for several years. Progress, however, has been slower than the optimism suggests. Digitization has moved faster in announcements than in actual rural loan origination, underwriting, and collections.

A closer look at the ground reveals why.

Connectivity Exists. Usability Does Not.

Rural internet penetration in India now stands at approximately 37%, and 4G coverage reaches close to 95% of the population. These figures are frequently cited as evidence that the infrastructure barrier is largely resolved.

The reality is more nuanced. Coverage is not the same as reliable connectivity. Consistent 4G speeds sufficient to complete a video-based KYC, upload property documents, or run an e-sign flow remain inconsistent across large parts of Tier 3 and rural India. The ASER 2024 survey found that while smartphone access among rural youth is high, only a fraction could bring a device with strong enough connectivity to complete basic digital tasks. In states like Bihar, Odisha, and Jharkhand, this gap is more pronounced.

Beyond connectivity, digital literacy among rural borrowers above 30 remains a structural constraint. Consider what a standard digital home loan journey requires:

For a first-generation smartphone user in a semi-literate household, this process frequently requires a human intermediary. Removing that intermediary entirely in the name of digital efficiency does not reduce friction. It transfers that friction to the borrower, and many simply drop off.

The Cash Economy Is Not Going Away Quietly

India’s rural economy remains substantially cash-based. Agricultural income, daily wage labour, small trade, and contract work are often received and spent in cash, with limited or irregular formal account deposits. This is not a temporary gap that will resolve with time. It reflects how transactions have operated across rural India for generations.

For digital underwriting models, this is a fundamental challenge. Bank statement analysis, cash-flow based underwriting, and Account Aggregator frameworks all depend on income being visible in a formal account. When a borrower earns Rs. 35,000 a month but deposits Rs. 8,000, the financial statement looks like a thin-file risk. The actual repayment capacity is invisible to the algorithm.

Lenders attempting to digitize rural credit underwriting must contend with a data environment that was not built around this population. Forcing urban data logic onto rural borrower profiles does not improve accuracy. It systematically excludes creditworthy applicants.

Unit Economics That Do Not Yet Add Up

The cost of acquiring and underwriting a rural home loan borrower remains significantly higher than the fee income and spread generated on small-ticket disbursements. Rural home loan ticket sizes typically range from Rs. 5 lakh to Rs. 15 lakh. Mahindra Rural Housing Finance, one of the more established players in this segment, has been actively diversifying upward into the Rs. 5-10 lakh range precisely because the economics of sub-Rs. 5 lakh loans are difficult to sustain at scale.

In urban digital lending, low customer acquisition costs and standardized underwriting make thin margins workable. In rural origination, field visits, physical document verification, local language support, and agent networks create cost structures that digital tools have not yet been able to compress to the required level.

This creates a paradox: the segment that most needs affordable credit is also the segment where lending cost ratios are highest. Until rural distribution unit economics improve meaningfully, many institutions will continue to concentrate digital investment in urban and peri-urban markets where returns are faster and cleaner.

Trust Is Still Mediated by People, Not Platforms

Rural borrowers have a well-founded scepticism toward institutions they have no prior relationship with. A digital lending interface, no matter how well designed, does not carry the same credibility as a known local agent or a branch relationship manager who has served the same family across two loan cycles.

This trust deficit is not irrational. It reflects historical experiences with predatory lending, opaque loan terms, and aggressive recovery practices in informal markets. When a rural borrower receives a digital loan offer with an interest rate expressed as a monthly flat rate rather than reducing balance, or encounters undisclosed processing charges at disbursement, the damage to institutional trust extends beyond that individual lender.

DSA and business correspondent networks continue to serve as the primary trust bridge in rural credit. Rather than viewing these intermediaries as inefficiencies to be eliminated, HFCs and NBFCs operating in rural markets have found them essential. Digitizing the agent experience, rather than digitizing around the agent, may be a more realistic path forward.

The Underwriting Data Problem Is Structural

Beyond connectivity and trust, rural credit underwriting faces a data availability problem that existing digital infrastructure has not fully solved. Bureau penetration remains low in rural India. Property records are incomplete, disputed, or not digitized in many districts. Income documentation for agricultural and informal workers does not conform to the ITR-based verification norms that digital lending platforms default to.

The Account Aggregator framework, which holds significant promise for cash-flow based underwriting, is still in early adoption stages across rural India. As of 2024-25, AA-linked consent flows work reliably for salaried urban borrowers with well-maintained accounts. For a rural borrower with multiple bank accounts, irregular deposits, and agricultural income flowing through a cooperative or PM-Kisan credit, the framework requires significant customization before it yields meaningful underwriting signal.

KCC digitization has improved agricultural credit access for existing borrowers, with over 7.75 crore Kisan Credit Card accounts operational as of 2024. But the transition from KCC data to broader credit underwriting for rural housing or MSME loans requires interoperability and data-sharing frameworks that are still being built.

What Needs to Change

Rural credit digitization is not failing. It is progressing at the pace that the underlying infrastructure and borrower environment actually allow. Institutions that acknowledge this distinction will build more durable rural strategies than those still projecting urban digital penetration curves onto Bharat timelines.

HFCs and NBFCs that want to build genuine rural lending capability need to move on a few fronts:

The institutions that crack rural credit will not be those that simply deploy urban fintech models in smaller towns. They will be those that treat rural underwriting as a distinct capability to be built, not a market segment to be served through diluted urban infrastructure.

The question is no longer whether rural India can be a viable credit market.

It is increasingly: are lenders building the right capabilities to serve it well, or are they waiting for rural India to eventually resemble the borrower profiles they already know?

The institutions that answer that question honestly will define the next growth frontier in Indian lending.